Introduction

Budgeting is like creating a road map for your finances.

It enables you to spend your money sensibly, achieve your financial goals, and minimize stress.

This beginner's guide will get you started or help you recover control of your spending.

1. Calculate Your Monthly Income

Determine your after-tax income before you start budgeting.

If you get a regular paycheck, that is probably your take-home money.

To gain a true picture of your finances, add back in any automatic deductions (such as 401(k) contributions or health insurance).

If you have additional income sources (such as side gigs), deduct any taxes or business expenditures.

2. Choose a Budgeting Method

Several budgeting methods exist, but let’s start with a simple one: the 50/30/20 rule:

Needs (50%): Allocate up to 50% of your income for necessities like housing, utilities, groceries, and debt minimums.

Wants (30%): Reserve 30% for discretionary spending—things you enjoy but don’t necessarily need.

Savings and Debt Repayment (20%): Commit 20% to building an emergency fund, saving for the future, and paying off debt beyond minimum payments.

3. Track Your Progress

Track your spending or use online budgeting tools. Regularly check in to see how you're doing.

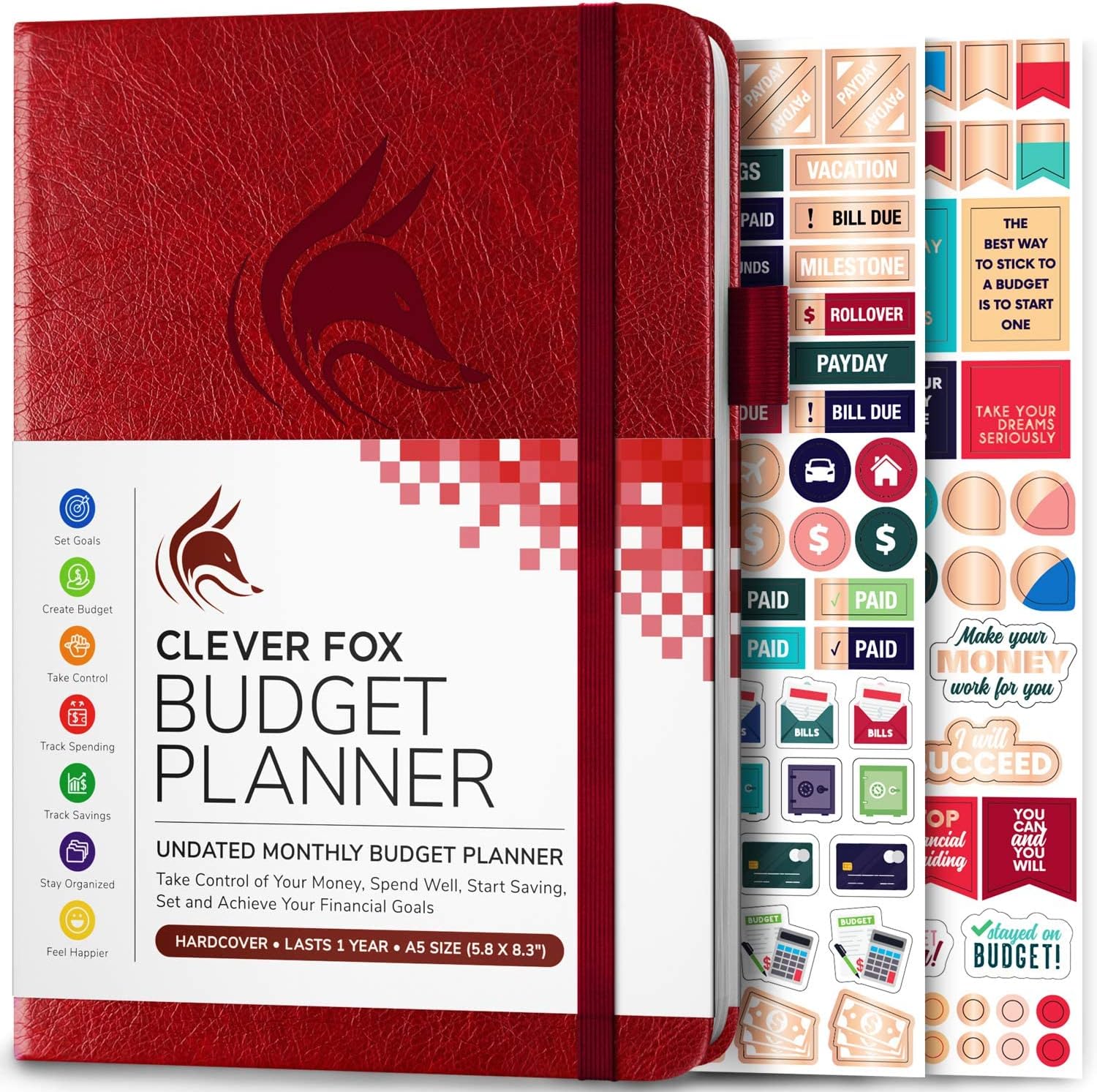

Budgeting is not a one-time exercise; it is a continuous process. Using a budget planner will help with this!

4. Automate Your Savings

Make saving easy by automating it. Set up automatic transfers to your savings or retirement accounts.

This ensures that your allotted funds get at their intended destination without the need for additional work.

5. Practice Budget Management

Your income, spending, and priorities will shift over time.

Review your budget on a regular basis—perhaps once a quarter—and make any necessary adjustments.

If you find it difficult to stick to your plan, consider these budgeting tips:

Use the zero-based budgeting system, which assigns each dollar a specific purpose.

Save before spending: Prioritize saving as soon as you get your salary.

Overestimate your food budget: Unexpected expenses occur, particularly with groceries.

Reconcile your budget daily. Keep track of your purchasing patterns.

Involve your spouse or partner: Budgeting is a collaborative effort.

Set exciting financial goals: Having a purpose drives you to stay to your budget.

Organizing your money is also an effective technique!

As Dave Ramsey advises, "Make your money work for you!" "Make a plan for every dollar."

Your income, spending, and priorities will shift over time. Review your budget on a regular basis—perhaps once a quarter—and make any necessary adjustments.

If you find it difficult to stick to your plan, consider these budgeting tips:

Use the zero-based budgeting system, which assigns each dollar a specific purpose.

Save before spending: Prioritize saving as soon as you get your salary.

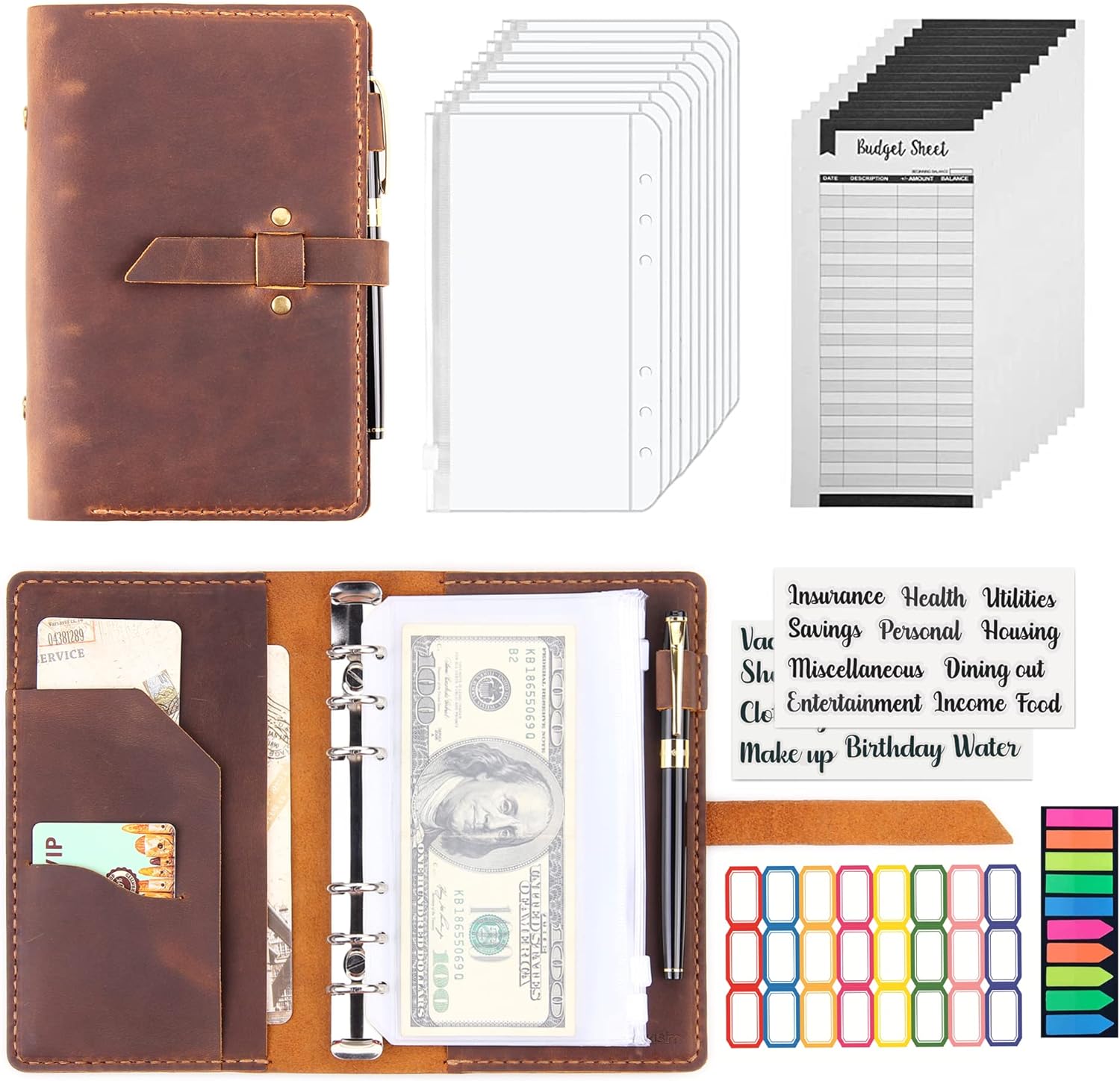

Organizing your cash will also assist you to understand where each dollar goes, and each dollar serves a function!

Here are a couple cash envelopes that will definitely help you arrange your money.

Leather-Hand Stitched-Budget Binder

Zodiac Budget Binder

Conclusion

Budgeting is about empowerment, not constraint. Making a budget gives you control over your money, reduces stress, and paves the way for financial success. Start now and watch your financial freedom develop!

Remember, every dollar counts, and your budget is your financial superpower. 🌟💰

Dave Ramsey’s The 7 Baby Steps: A Proven Path to Financial Success

Dave Ramsey's core money management strategy centered around the 7 Baby Steps.

These steps lay forth a detailed plan for obtaining financial stability, removing debt, and increasing wealth. Let's investigate them:

Save $1,000 for Your Starter Emergency Fund:

Begin by setting aside $1,000 as your initial emergency fund. This fund acts as a safety net for unexpected expenses.

Pay Off All Debt (Except Your Mortgage):

Focus on eliminating non-mortgage debt using the debt snowball method. Start with the smallest debt and work your way up.

Save 3–6 Months of Expenses in Your Fully Funded Emergency Fund:

Build a robust emergency fund to cover living expenses for 3–6 months. This fund provides peace of mind during job loss or other crises.

Invest 15% of Your Household Income in Retirement Accounts:

Allocate 15% of your income toward retirement savings. Maximize contributions to employer-sponsored plans like 401(k)s and IRAs.

Save for Your Children’s College Fund:

If you have children, start saving for their education. Consider 529 plans or other tax-advantaged accounts.

Pay Off Your Home Early:

Accelerate mortgage payments to become debt-free, including your home. Imagine the financial freedom of owning your house outright!

Build Wealth and Give Generously:

Once you’ve achieved financial stability, focus on building wealth through investments, real estate, and other income streams.

Use your wealth to make a positive impact by giving generously to causes you care about.

Whether you're just getting started with your finances or need a fresh start, Dave Ramsey's advice can help you achieve financial stability and prosperity.

Remember, it is never too late to take charge of your finances and change your future! 🌟💰

Comments

Post a Comment